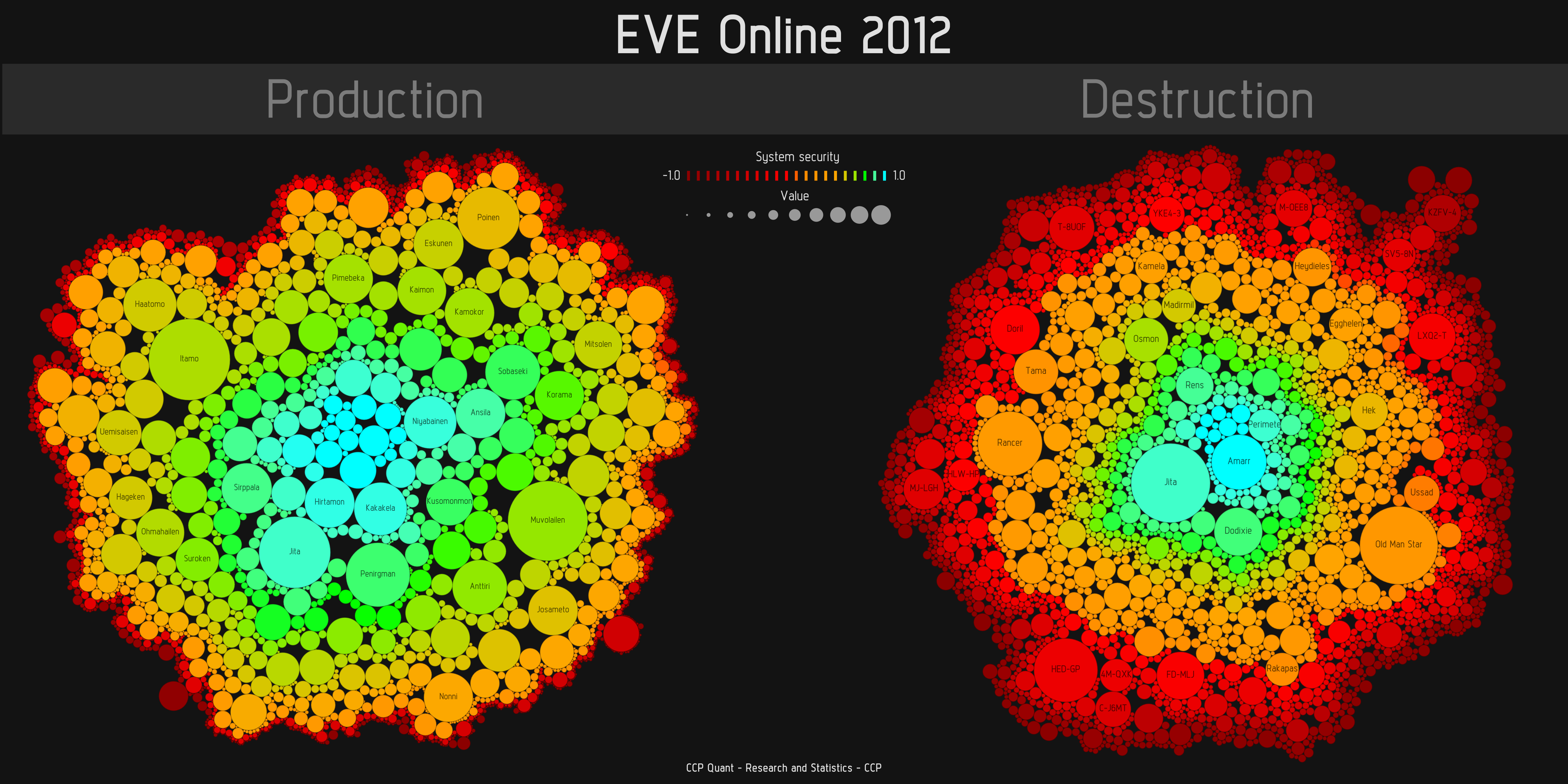

+Doyce Testerman posted up an expanded version of the "Creation v. Destruction" graphic featured at the EVE keynote, and I was inspired to write some more words on the subject:

|

| Image source: CCP |

0.0 Industry Buff Has Arrived

This topic was pretty hot this fall. I wrote some words on the matter, again from my T2 perspective at the time. But as a brief TL;DR

The problems facing null industry are many faceted. Material supply and outpost limitations were two parts of that problem. There are more issues when it comes to bringing T2 production out to the warzone, leaving freight-from-HS as the more desired solution.The meat-and-potatoes, as I see it? This is an excellent first step. By improving low-end volumes locally, and vastly improving outpost hardware, this goes a very long way to improve the industrial picture. It's starting to look like a well-implemented plan to drop outposts strategically for carebear contingents could see some real successes.

The other part I see here is a great start toward farms-and-fields. By incentivizing people to utilize player-owned outposts as manufacturing hubs puts more carebear skin in the game and makes conquering that resource a painful (but avoidable) blow. I have yet to do any real number-crunching, but it's giving me hope to try whereas today I wouldn't even consider the proposition.

- BUT -

These improvements really make the T1/Capital picture juicy... but still leaves a lot to be desired for T2. And I'd argue that the T2 module stream is just as important as the T1 hull stream. Also, I'd argue that there will be an "unintened consequence" where traditional compression drops the price of low-ends in empire significantly... but that might be a good thing.

There are a lot of problems with the T2 paradigm that don't fit well into a null-bear strategy, and maybe that's "working as intended". The primary problem is that moon-goo is regional, and you won't be able to source more than a few advanced-materials locally. If you're stuck shipping anyway, why bother taking the extra risk of DIY when you can just ship in the final products? Also, Invention is centered around high-volume, low diversity. You'd still be stuck exporting the majority of finished products. Lastly, datacores are an empire product, once again requiring shipment. This leaves "ship it" three votes ahead of "build it". Especially when logistical effort is really tallied.

- But, BUT -

I don't want to pooh-pooh the whole picture. Odyssey gives us industrialists the first REAL chance to carve out a player-owned factory-fortress. By dropping a few outposts, strategically, deep inside your controlled territory, you could do some really interesting work. T2 would not be out of the picture, and might be a great way to leverage moon revenue and put the plebes to work. There's still a problem of POS being a little too squishy for my taste, but I think the tools are being rolled out to give a damned good roll of it.

This is just a first reaction, and no real number crunching has been put behind it. I am intrigued by the actual mechanical feasibility. More thoughts soon(tm)